Africa has witnessed the world’s fastest increase in e-connectivity in recent years. Yet, with only around a quarter of its population with internet access, Ocorian Directors John Félicité and Novan Maharahaje analyse why the continent’s digital divide could continue to expand whilst highlighting the role of private sector financing and corporate governance in helping to bridge the gap.

Despite Africa’s recurring growth narratives and noteworthy progress in various economic sectors, income inequality is still a major hurdle to social advancement on the continent. A report issued in September 2019 by the United Nations Conference on Trade and Development (UNCTAD) warns that Africa’s inequality could worsen unless concrete action is taken to bridge the continent’s digital divide – the gap between people with internet access and those without.

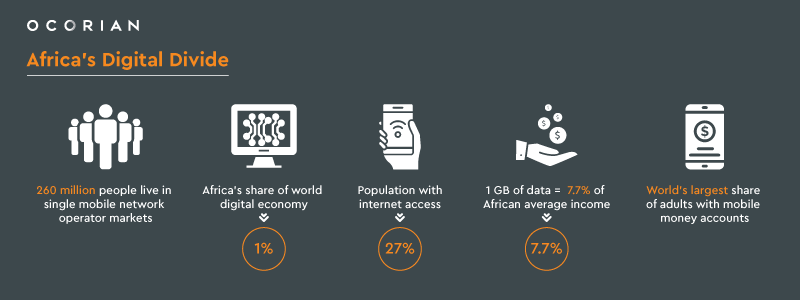

The worldwide digital economy is currently estimated at 15.5% of global GDP. Dominated by the United States and China, Latin America and Africa trail considerably behind. At less than one percent, Africa’s estimated share of the global digital economy is negligible and could shrink further in the absence of accessible and affordable internet.

Africa still lags far behind for internet access

With the highest recorded growth globally in internet access – up from 2.1% in 2005 to 24.4% in 2018[i] – it is true that the continent has made great strides in terms of e-connectivity. However, with only 27%[ii] of the continent’s population with internet access, Africa still lags behind the rest of the world. The problem is exacerbated by accessibility figures of around 90% in North America and Europe.

Africa’s low rate of internet access is impacting its ranking on other related indices such as e-commerce readiness. In 2018, UNCTAD established that Africa was home to nine of the ten countries the least prepared for e-commerce adoption.

When internet is accessible in Africa, its affordability is often constrained by a lack of competition. According to the Alliance for Affordable Internet (A4AI), the trend for broadband to become more competitive is slowing down in many African countries. A4AI estimates that across sub-Saharan Africa, some 260 million people live in markets dominated by just one major mobile network operator. This is an area where both development finance institutions and private investors could play a critical role. They could back local bandwidth providers and SMEs in the telecoms sector whilst supporting local institutional investors such as banks and pension funds.

Lack of competition is having a huge impact on accessibility and affordability

Understandably, the lack of choice has a huge impact not only on accessibility but also on affordability. Across sub-Saharan Africa, people living in markets where there is a lack of competition could on average be paying an additional 5.83% of their monthly income for just 1 GB, reports A4AI in its 2019 Affordability Report (the Report).

The problem of a persistently high cost for internet is not confined to Africa. In low and middle-income countries, 1 GB of data equates to 4.7% of average income – more than double the UN threshold for internet affordability. However, according to the Report, this figure rises to 7.7% across Africa, making the internet out of reach for millions.

What impact could bridging Africa’s digital divide have?

Bridging the digital divide could transform Africa’s societies. The jobs and wealth created by digitised nations could trickle down to a large number of sectors, of which health, transport, energy and agriculture stand to gain the most.

We are already witnessing the positive impact of digitalisation in many areas, one of the most palpable being fintech. On a continental scale, Africa boasts the largest share of adults with mobile money accounts in the world. It is also true that over the last few years, Africa’s tech ecosystem has grown multi-fold, with new incubators, accelerators and start-ups sprouting almost on a daily basis. Yet, where countries such as Kenya have a seemingly thriving tech and mobile money ecosystem, there is no genuine scale across the continent.

It is clear that there is still a lot to be done to curb the digital divide in Africa. The economic impact of digital technology depends on factors such as governance, education, skills levels and basic infrastructure – the International Energy Agency claim that bringing reliable electricity to all Africans would require annual investment of around $120 billion through to 2040. However, by enhancing competition, mitigating risks and boosting private sector financing namely through private equity and blended capital, the pressing need to make internet more accessible and affordable across Africa stands a chance of being realised.

Supporting the growth of tech companies

At Ocorian, we have been privileged to assist in the setting up and growth of leading technology firms and start-ups in Africa across the mobile money, digital bank, micro finance and lending and internet backend infrastructure landscapes. This places us in a unique position to understand the critical success factors and market dynamics across some of Africa’s leading technology-led industries.

From inception through to maturity, we help tech companies measure and enhance their enterprise value and investor value, ensuring they have the required finance capital and governance capital for their optimal growth.

Find out more about Ocorian’s International Growth & Advisory Services here.