Kemi Owonubi, Head Corporate Finance, RMB Nigeria shares her thoughts on the future of the West African Corporate Finance Market.

The economic and social impact of the COVID-19 pandemic continues to be felt globally. In West Africa, beyond a health crisis, the economic aftershocks will continue to be felt through reduced foreign trade and investment, and declining local income and reduced consumption levels.

Our regional economies are predominantly reliant on commodity exports, which are exposed to price volatilities and changes in global supply & demand dynamics. Oil & Gas commodity exporting countries like Nigeria and Ghana, have been significantly impacted by dampened prospects for a near term recovery in oil prices; and with Cote d’Ivoire, face supply chain disruptions and forecast lower demand for agricultural commodity exports like cocoa, due to weakened global consumer demand. The impact of the pandemic is also felt on tourism and travel, given the restrictions on movement and drastic reductions in labour force on the back of the downturn. It is within this context, that we reflect on the prospects for West African mergers and acquisitions (“M&A”).

Pre COVID-19 M&A outlook[1]

The top five sectors for M&A in 2019 were energy and power, media and entertainment, fast-moving consumer goods (FMCG), real estate, and industrial materials. The total value of announced M&A deals by value in 2019 (for Sub-Saharan Africa) was $79.6 billion, a 142% increase over the 2018 value. All the above-listed sectors, except for media and entertainment, feature consistently in the rankings each year. 7 of the top 10 acquisitions (which were all strategic, company-led deals), were cross geography transactions, that enabled the acquirer to expand its business, into the target’s country and region.

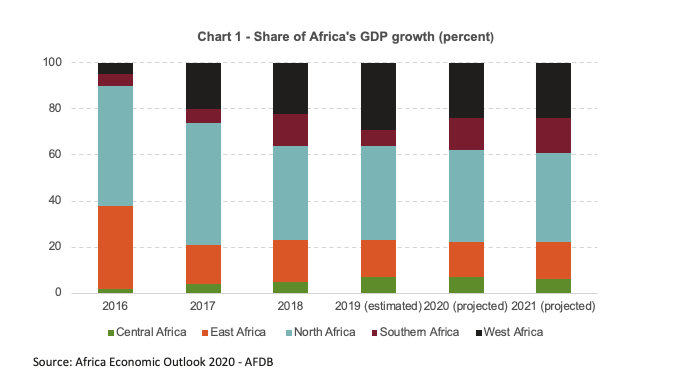

Pre-COVID-19 regional outlook

The African economic outlook for 2020 was similar to 2019. Real GDP growth was estimated at 3.4% for 2019 and projected to accelerate to 3.9% for 2020[2]. Leading the way were six economies, amongst the world’s ten fastest growers, including the three West African nations of Ghana, Cote d’Ivoire and Benin (See Chart 1).

Positive investor sentiment in Africa was growing supported by improving macro and political conditions and favourable population demographics. Appreciable deal activity was expected in broad-based energy and power, FMCG and financial services sectors, telecommunications, media and entertainment.

The adjusted regional outlook

Deal activity is typically a direct result of underlying corporate performance (within the context of the macro fundamentals), growth prospects and the availability of well-priced capital. The 2020 GDP outlook for sub-Saharan Africa is expected to contract and has been revised downwards to between -2.1% and -5.1%.

M&A post-COVID

We anticipate that the conditions created by COVID-19 will present select opportunities for the discerning investor, who must be prepared to take advantage of such opportunities once they appear or are created. Such opportunities will include restructurings, bargains involving distressed sales, or as new segments and businesses, that emerge from opportunities presented by disruptions to existing business models.

Relative to a pre-COVID world, where M&A was broadly directed by the objectives of scale, and driven by economic optimism, in the post-COVID world, M&A will become to some extent, a tool for survival, given the constraints on capital, and the requirements for cost control and optimisation. There will be opportunities for domestic companies with strong balance sheets & cashflows, and for companies outside the region looking to expand geographically, with the prospects to acquire assets at favourable price levels.

This is how we anticipate that the sectors will be affected.

The Non-Discretionary sectors

Non-Discretionary sectors within (i) Consumer Goods – food, grocery retail, personal and home care (ii) Healthcare – manufacture and retail of pharma products, healthcare infrastructure including hospitals and diagnostics (iii) Telecommunications – communications including voice and data, telecoms infrastructure; and (iv) Logistics and Transportation – distribution infrastructure, warehousing.

These sectors will experience varying levels of impact, due to the pandemic. There will be opportunities to leverage and improve their business and operational models, to take advantage of the opportunities presented, through organic improvements, vertical acquisitions across the value chain or opportunistic acquisitions to build scale.

There is an especially positive outlook for local manufacturers in countries with a high import bill for consumer products. This is so as import substitution becomes a big theme, due to severely reduced FX earnings for governments. A depreciated currency, a trade deficit position and declining reserves will mean countries can no longer support non-essential imports. This presents an opportunity for local manufacturers to produce better quality goods (for sale to an existing consumer market), at higher price levels, capturing higher margins.

The Discretionary sectors

Discretionary sectors such as (i) Travel and Leisure – tourism, hospitality, aviation (ii) Real Estate – residential, commercial (iii) Construction (iv) Discretionary Retail (v) Non-Essential Financial Services (vi) Media and Entertainment – cinemas and theatres; and (vii) Oil and Gas – upstream and related services. These sectors have been impacted by declining incomes and levels of activity due to the restrictions to movements. We expect these sectors will likely only see a return to “normalcy” in the latter half of 2021, or even later, depending on the depth, impact and duration of the economic effects of the COVID-19 pandemic.

The Innovation and Technology-enabled sectors

Tech-enabled sectors such as (i) E-Commerce – including online retail, tech-enabled logistics and transportation (ii) Digital Financial services – including consumer lending platforms & Payment Platforms (iii) Media and entertainment – over the top (“OTT”) platforms (iv) Digital Education; and (v) ICT – Security and IT software solutions. Businesses in these sectors are evolving into high-value high-growth companies, driven by technology, and further enhanced by the solutions they provide to COVID-19 related challenges.

Where to next?

Despite the adjusted outlook, we still see the opportunity for sizeable M&A deals in the non-discretionary sectors, as demand will be relatively resilient across critical sectors such as healthcare, grocery and food retail, other consumer staples, telecommunications and logistics. Companies in the discretionary sectors, who entered the crisis with high leverage levels, may present bargains for investors, with restructurings, and where the business is a good fit into their existing strategy. There will also be consolidation opportunities, fueled by a need to survive. We anticipate a general realignment of property prices in the real estate sector, as investment properties are realised for more optimal uses of cash.

We envision deals in the emerging tech enabled sectors, though some may still be in the early phase of growth to be sizeable. On a upside, growth in technology enabled businesses will be accelerated by the newer, growing needs of a post-COVID consumer.

In conclusion, M&A will remain active. We believe that while the typically deal heavy sectors may slow down, activity will continue, driven by value opportunities and consolidations. Overall, West Africa remains a resilient region, and will respond to the challenges at hand with astuteness and innovation.

[1] Refinitiv Deals Intelligence – SSA African Investment Banking Review – FY 2019

[2] Africa Economic Outlook 2020 – African Development Bank Group, Outlook model assumptions included average of $63 oil prices in 2020.